Trump’s Fiscal Legacy: A Comprehensive Overview of Spending, Taxes, and Deficits

A Full Accounting of Trump's Fiscal Impact

President Donald Trump’s tax, spending, and deficit legacy is still being defined. Critics point out that Trump’s tax cuts and spending increases led to a $3 trillion budget deficit. They note that Trump’s presidency saw the debt surpass 100% of the economy, even though he came into office with a healthy economy, declining interest rates, and relative peace after 15 years of global military conflict.

On the other hand, the president’s defenders respond that he inherited large budget deficits that were already projected to grow on autopilot due to escalating Social Security and Medicare costs. They argue that the 2017 tax cuts contributed heavily to the growing economy through 2019. Finally, they note that the president repeatedly proposed budgets with significant deficit reduction but was thwarted by a bipartisan congressional majority that aggressively supported expensive new initiatives, as well as by a global pandemic that virtually everyone agreed required a massive federal response.

The end of Trump’s presidency allows for a final assessment of his tax, spending, and deficit record. As the methodology section explains, this analysis begins with the 10-year budget baseline that President Trump inherited in January 2017 and measures all subsequent tax and spending changes through the February 2021 baseline, which was released as the president left office. The analysis is based on more than a dozen Congressional Budget Office (CBO) baseline updates over these four years, supplemented with the line-item scores of all notable bills signed into law by President Trump.[1]

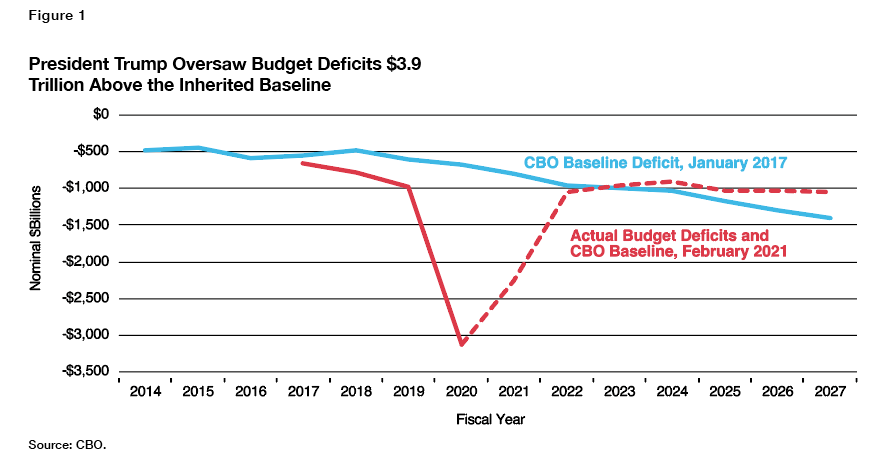

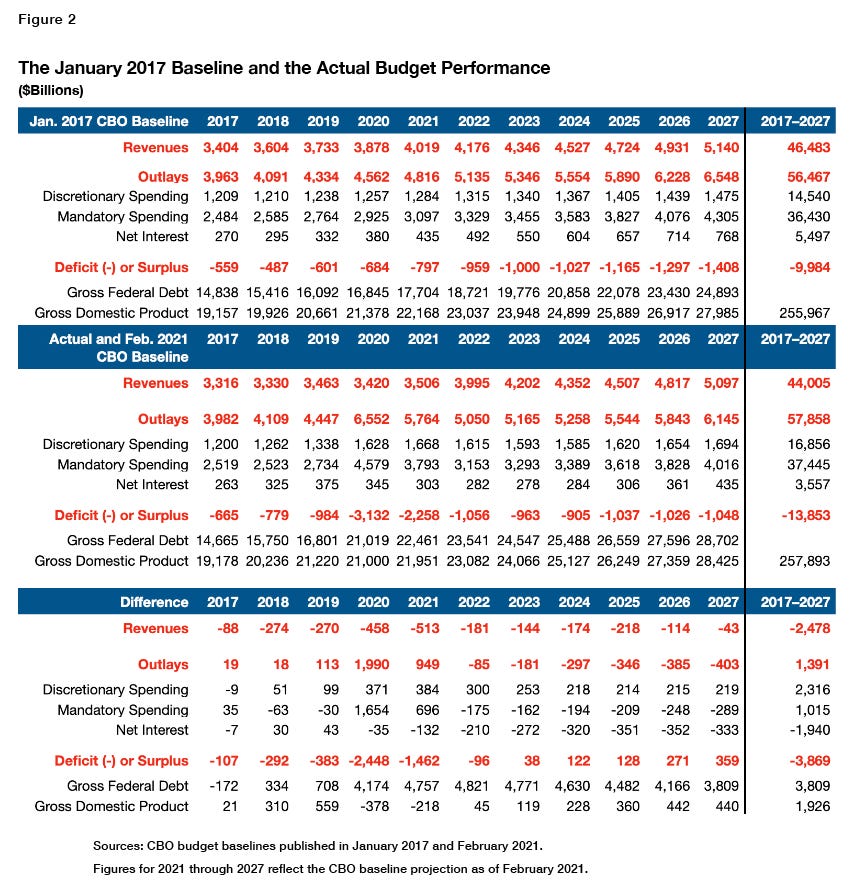

When President Trump entered the Oval Office, CBO projected the cumulative 2017–2027 budget deficits would be $10.0 trillion. When he left office four years later, CBO’s projected deficits for the same period were $13.9 trillion. The president signed or enacted $7.8 trillion in new initiatives, the costs of which were partially offset by $3.9 trillion saved from economic growth revenues and technical re-estimates of taxes and spending levels.

Economic and technical factors produced a substantial $3.9 trillion in actual and projected savings over this period. Of this amount, $2.7 trillion comes from falling interest rate projections, which reduced the projected cost of net interest on the national debt. Another $1.3 trillion comes from higher tax revenues produced by faster economic growth projections. Technical re-estimates have reduced mandatory spending projections but also tax revenues. Most of these savings are projected to occur later in the 2017–2027 period and thus may not materialize if economic growth slows or interest rates rise.

President Trump signed legislation and approved executive actions costing $7.8 trillion over the decade—compared to $5.0 trillion for President Obama and $6.9 trillion for President Bush, and he enacted these costs in just a single four-year presidential term, compared to his predecessors’ eight years in the Oval Office. The largest drivers were pandemic relief legislation ($3.9 trillion), the 2017 tax cuts ($2.0 trillion), and legislation raising the discretionary spending caps ($1.6 trillion).

President Trump’s four annual budget proposals were scored as reducing budget deficits by $2.4 trillion over the subsequent 10 years. Nearly all proposed savings came from repealing and replacing Obamacare, as well as vague promises to cut domestic discretionary spending nearly in half. Outside of the budget documents, President Trump did not aggressively push either initiative after 2017.

Trump left the White House with the largest peacetime budget deficit in American history and a national debt exceeding 100% of the economy for the first time since World War II. The failure to address unsustainable Social Security and Medicare costs leaves a projected 30-year baseline deficit of $112 trillion.

$3.9 Trillion in Additional Deficits

When President Trump took office in January 2017, he inherited a growing economy and budget deficits that had gradually fallen to 3% of GDP in the years since the Great Recession. At this time, the Congressional Budget Office (CBO) projected that the $585 billion budget deficit from 2016 would dip to $487 billion by 2018, before the baby boomer–driven rise in Social Security and Medicare costs would gradually push deficits up to $1.4 trillion by 2027. Overall, CBO projected that $10.0 trillion in deficits over the 2017–2027 period would drive the debt held by the public to $24.9 trillion (see Figures 1 and 2).[2]

Yet while running for president, Trump pledged to balance the budget and then pay off the entire national debt. He boasted to the Washington Post’s Bob Woodward, “we’ve got to get rid of the $19 trillion in debt … I think I could do it fairly quickly … I would say over a period of eight years.”[3] Of course, doing so would be virtually impossible—politically, economically, and mathematically—especially given his promise not to cut Social Security and Medicare, which drove virtually the entire projected rise in debt. Trump’s plan to achieve nearly $25 trillion in 10-year savings consisted of renegotiating trade deals, bringing overseas companies (and their taxes) back to America, repealing Obamacare, and growing the economy. While paying off the debt within a decade was an absurd promise, serious deficit reduction was possible given the growing economy, falling defense costs, and a unified Republican Congress that had long promoted significant entitlement reform.

Instead, as Trump left office, the 2017–2027 budget deficits were estimated at $13.9 trillion—$3.9 trillion higher than the inherited projection. During each of Trump’s four years in the White House, the actual deficit exceeded the original CBO’s projections by at least $100 billion. For the first time in American history, the deficit in fiscal year 2020—amid a massive bipartisan fiscal response to the pandemic—reached $3 trillion (accounting for 14.9% of GDP, a level that has been exceeded only during the height of World War II).

The president left office with a $2.3 trillion deficit projected for 2021. Potential budget savings forecast for the 2022 through 2027 period are driven by the expiration of expensive legislation as well as economic and technical re-estimates, not by any deficit-reduction legislation signed by President Trump.