How Higher Interest Rates Could Push Washington Toward a Federal Debt Crisis

Why Rates May Rise - And What it Would Cost

(Originally published by the Manhattan Institute)

(NOTE: When this report was released in 2021, the economic commentariat responded with overwhelming dismissal and even mockery. Critics asserted that 15 years of low interest rates would surely continue, so there was no reason to constrain Washington’s deficit-spending appetite. Needless to say, subsequent events have vindicated this report).

Today’s trendy economic argument asserts that the current debt-to-GDP ratio of 100% has not harmed the economy, and therefore Congress can easily afford large new government expansions. But that argument has two fatal flaws. First, it fails to acknowledge that over the next few decades—even without new legislation—the debt is already projected to reach levels that even debt doves would likely consider unsustainable. Second, this argument assumes that interest rates will forever remain near today’s low levels, thus minimizing Washington’s cost of servicing this debt. However, economic trends rarely remain linear indefinitely, and interest-rate movements have rarely followed forecaster projections. Indeed, several realistic economic scenarios could easily push interest rates back up to 4%–5% within a few decades—which would coincide with a projected debt surge to greatly increase federal budget interest costs. Debt doves have no backup plan for this possibility. Policymakers should now enact reforms that scale back the escalating long-term debt projections in order to limit the federal government’s risk exposure to a fiscal crisis.

Introduction

Congress and the White House are engaging in the largest borrow-and-spending spree since World War II. The $3 trillion legislative response to the pandemic was largely justified but nonetheless staggering in its size: at 15% of GDP, it exceeded the 1930s New Deal response to the Great Depression. Yet this deficit spending was just a warm-up to President Biden and Congress’s even more ambitious agenda. They have already enacted a $1.9 trillion stimulus bill and a $550 billion infrastructure bill, and adding proposals like Build Back Better ($3 trillion in deficits assuming Congress repeals the fake expiration dates), [1] and new discretionary spending ($1 trillion over the decade) would add up to $6.5 trillion in additional ten-year debt from one year of legislation. This is quadruple the cost of the 2017 tax cuts, and it exceeds 20 years of domestic and international costs related to the war on terrorism. Nor are Democrats finished yet, as President Biden still has campaign pledges related to health care, Social Security, education, and other areas that would add an additional $3 trillion in debt. [2]

This deficit spending would take place on top of growing baseline deficits and push the national debt—less than $17 trillion before the pandemic—past $44 trillion a decade from now. And the debt would continue growing thereafter as the result of $112 trillion in 30-year baseline deficits, driven largely by deepening Social Security and Medicare shortfalls. [3] In other words, the U.S. government is in the early stages of what is projected to be the largest government debt binge in world history.

Yet there has been no widespread backlash. There is no tea party movement, or Ross Perot– style political candidate warning America about unrestrained red ink. Congressional Republicans have gone largely silent on this historic borrowing spree, and polling by the Pew Research Center shows the public’s budget deficit concerns plummeting over the past decade. [4] Financial markets have shrugged off this surging debt. Most surprisingly, even economists have heralded this new era of red ink. Leading mainstream Democratic economists Jason Furman and Lawrence Summers have written: “Washington should end its debt obsession,” [5] while Trump economic advisor and noted conservative tax cutter Lawrence Kudlow has called the debt “quite manageable” and not “a huge problem right now at all.” [6]

This newfound acceptance of surging government debt is largely based on two highly questionable assumptions.

First, economists have asserted that fiscal consolidation is unnecessary because Washington’s current debt level of 100% of GDP has not proved unaffordable or economically damaging. Leading economists have asserted that expensive new fiscal expansions are justified until the debt reaches 150% of GDP. [7] Yet this framework fails to take into account that Washington is already projected by the Congressional Budget Office (CBO) to run $112 trillion in additional baseline deficits over the next three decades, which will push the debt past 200% of GDP. At that point, annual deficits are projected to top 13% of the economy (the equivalent of nearly $3 trillion today), and interest payments on the debt would be the largest federal expenditure, consuming nearly half of all tax revenues. [8] Adding all of President Biden’s budget proposals would push the debt past 250% of the economy in three decades. And instead of leveling off, the baseline debt would continue expanding by 80% of GDP per decade. In short, the baseline debt is already projected to grow to unsustainable levels even before any new proposals are enacted.

The second questionable assumption that the debt doves make is that today’s low interest rates paid on this debt will continue forever. The average interest rate paid on the national debt has fallen from 8.4% to 1.4% since 1990. [9] This decline was not forecast by economists, and many disagree on its specific cause. Yet many economic commentators have expressed an unshakable confidence that relatively low interest rates will essentially continue forever. If they are wrong, the combustible combination of surging debt and rising interest rates at any point in the future would risk a debt crisis. Even interest rates of 5% could push the national debt toward 300% of GDP within three decades, if paired with modest new fiscal expansions in the meantime. Both the poor historical record of economic forecasters as well as the tendency of economic variables like interest rates to fluctuate over the long term should give pause to policymakers, taxpayers, and economists when examining Washington’s rapidly rising debt projections.

The purpose of this report is to more deeply examine the threat that higher interest rates would pose on Washington’s long-term fiscal sustainability. First, it examines the causes of the post- 1990 decline in interest rates and the factors likely to push interest rates upward over the next few decades. Next, it analyzes Washington’s steeply rising debt levels over the next several decades and how rising interest rates risk pushing government interest costs, annual budget deficits, and total government debt to unsustainable levels. The report concludes by calling on lawmakers to gradually pare back these baseline deficits and thus limit the likelihood of a future debt crisis.

I. The Interest-Rate Outlook

Nominal interest rates are the sum of the demanded real rate of return and a premium to account for inflation risk. After remaining steady during the 1950s through the late 1960s, interest rates accelerated in the 1970s but fell below zero in real terms because the actual inflation rates far exceeded the expected inflation rates that were built in to the nominal rates (see Figure 1). By the early 1980s, investors had learned their lesson and began demanding exorbitant nominal interest rates to compensate for high expected inflation and a premium to account for inflation risk. The Federal Reserve’s subsequent taming of inflation left 1980s real interest rates at historically high levels. A key lesson is that low and stable interest rates require market confidence in low inflation rates.

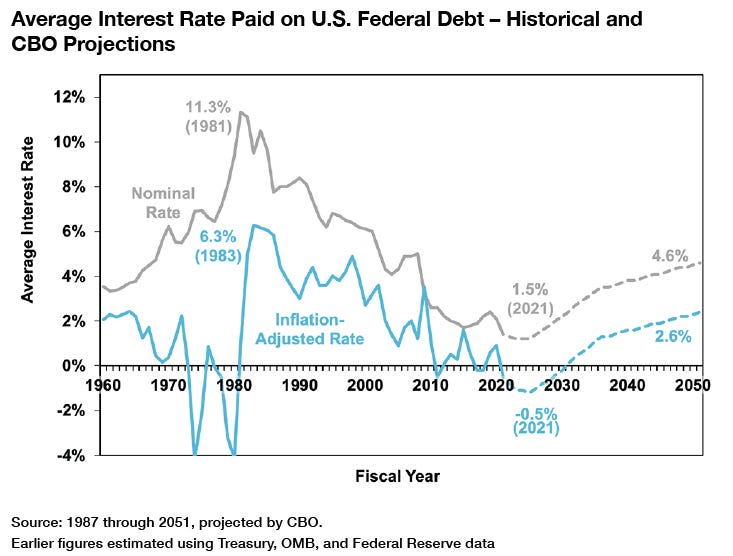

Figure 1

After the higher real and nominal rates of the 1980s, the federal government by 1990 had paid an 8.4% average interest rate on the debt held by the public. The average rate had gradually declined to 4.9% by 2006, before the housing collapse and financial crisis dropped rates further, to approximately 2.0%, where they remained until a recession and a wave of short-term pandemic borrowing decreased average debt maturities and dropped the average federal rate to its current level of 1.4%. [10] Although the Treasury has occasionally altered the average maturity of its debt, the average interest rate has closely tracked the average rate on the 10-year Treasury bond. AAA corporate bonds and mortgage rates have followed a similar path.

A key question is, what caused this steep 30-year decline in interest rates? Private economic forecasters as well as federal government forecasts produced by CBO and the White House Office of Management and Budget (OMB) have consistently failed to predict the interest-rate decline and, in fact, regularly predicted that rates would increase. In hindsight, economists have converged on some combination of several factors to explain the three-decade decline in interest rates: [11]

Demographics. The 74 million baby boomers began saving more for retirement in their 40s, 50s, and early 60s. At the same time, the population growth of younger adults in their prime borrowing years slowed down. Additionally, the general population growth slowdown in both the U.S. and abroad likely reduced productivity rates, incentives for research and development, and the need for expensive new investments to equip this smaller workforce.

Declining Productivity. The surprising decline in productivity, particularly since 2006, has reduced interest rates by reducing demand to borrow now against future (assumed) wealth, as well as by reducing the marginal product of capital and demand for new investments in the economy. A related possible factor has been the reduced need for physical capital investments brought on by the technology revolution (i.e., more Facebooks, fewer huge manufacturing factories) and better management techniques, helping companies become more efficient with existing capital.

Global Savings Glut. Former Federal Reserve Chairman Ben Bernanke has observed that global savings and investment soared in the early 2000s, collapsed after the financial crisis of 2007–09, and then resumed growth. [12] The decline in interest rates suggests that excess savings—rather than growing demand for investments—fueled this growth. However, much of the additional savings came from Asia and oil-exporting countries, and their glut seems to be slowing in recent years. [13]

Global Flight to Safety. Historic stock- and financial-market crashes in 2000, 2007–09, and again in early 2020 drove savers in the U.S. and abroad to seek out the safety and predictability (albeit with low returns) of U.S. Treasury bonds and related investments, such as AAA corporate bonds. Investment safety has been especially important for baby boomers approaching retirement and international investors worried about global market instability.

Global Economic Trends. The increasingly interconnected global economy has caused interest rates across countries to converge more than ever before. And the cross-nation replication of factors such as an aging population, global savings, and declining productivity has reinforced these interest-rate declines in most advanced economies.

Inflation Anchoring and Federal Reserve Policy. As stated above, central banks in the U.S. and abroad have taken a stronger, and more consistent, push for low inflation and monetary stability since the 1980s, which has reduced the inflation-risk premium in interest rates. Over the past 13 years, aggressive low-interest-rate policies and quantitative easing have further pushed short-term interest rates downward.

Private-Sector Deleveraging. After the 2007–09 financial crisis, many overextended families and businesses took steps to minimize their debt exposure. This has meant households increasing their savings and paying down debt, businesses shoring up their balance sheets, and lenders imposing tighter loan requirements. This deleveraging increased savings and reduced consumption and borrowing. It was also broadly disinflationary, further contributing to lower nominal interest rates.

Government Debt Still Raises Interest Rates

This three-decade reduction in interest rates may create the impression that rising government debt no longer puts upward pressure on interest rates. Standard economic theory has long held that government borrowing reduces the amount of savings available for the private sector to borrow and invest—which, in turn, raises the price of savings, or the interest rate. However, U.S. interest rates fell during a period in which the federal debt held by the public increased from 40% to 100% of GDP. Does that disprove the link between government debt and interest rates?

Extensive economic research maintains that the link still exists. In 2003 and again in 2007, Federal Reserve economist Thomas Laubach determined that, all else equal, a 1-percentage-point increase in the debt-to-GDP ratio increases interest rates by three or four basis points. [14] In 2004, economists Eric Engen and Glenn Hubbard calculated that “an increase in government debt equivalent to 1% of GDP would likely increase the real interest rate by about two to three basis points.” [15] More recently, a 2019 CBO study coauthored by Edward Gamber and John Seliski employed methodologies similar to those of Laubach and Engen/Hubbard to find a persistent two- to three-basis-point effect. [16] A 2019 analysis by current Biden administration economist Ernie Tedeschi found that “each percentage point increase in debt-to-GDP raises the 10-year yield by 4.2 basis points, all else equal.” [17]

This analysis suggests that the post-1990 increase in the federal debt ratio from 40% to 100% of GDP should have raised interest rates by 1.2–2.4 percentage points. Instead, real interest rates fell by 2.5 points. Squaring this circle lies in the final words of the previous paragraph: “all else equal.” The positive link between government debt and interest rates has not been eliminated but rather offset by other economic factors reducing interest rates. Jason Furman and Lawrence Summers concede that interest rates have been pushed upward by factors such as rising government debt and lower tax rates on capital investment. [18] So why have overall interest rates fallen? Because, citing earlier estimates by Summers and Lukasz Rachel, those offsetting factors reducing real interest rates across nations “declined by about 700 basis points.” [19] Tedeschi’s analysis also finds that many of the interest rate–dampening factors detailed above simply overwhelmed the upward pressure on interest rates caused by rising government borrowing.

Will Rising Debt’s Interest-Rate Effects Continue to Be Canceled Out?

It is tempting to conclude that—even if rising debt pushes interest rates upward—those offsetting factors will continue to hold down interest rates, liberating lawmakers to borrow without worry. Instead, these offsetting factors should be a source of caution because there is no guarantee that they will last. The federal government has much more long-term control over rising federal debt—which raises interest rates—than it does over the broader economic and global trends that have recently pushed interest rates downward. [20] These broader interest-rate trends (and resulting lower budget interest costs) have served as a substantial, accidental, and possibly temporary subsidy to heavy-borrowing federal lawmakers. It is dangerous to assume that these offsetting trends will continue forever.

Here’s a key point. Assuming that each percentage-point increase in the debt continues to raise interest rates by 3 basis points, the projected 100% debt-to-GDP increase over the next three decades should, all else equal, push interest rates up by 3 percentage points. [21] To maintain today’s low interest rates, therefore, it would not be enough for those offsetting factors to remain constant; they would have to accelerate even further, in order to drive an additional 3 percentage- point interest-rate decline.

An analogy would be a football team that managed to improve its overall win–loss record over several seasons—despite a rapidly worsening defense—because its offense kept improving enough to barely outscore its opponents. Claiming that the wins prove that defense no longer matters, or should be allowed to continue declining on the assumption that the offense will simply continue to improve even faster, is obviously unwise.

Other Factors May Also Raise Interest Rates

Is it wise to assume that offsetting factors can accelerate enough to overcome the factors that will push interest rates higher in the future? Should we assume, for example, that productivity growth rates will continue to fall closer to zero? Or that the global savings glut accelerates? The Federal Reserve already faces a zero lower bound on short-term interest rates. It is not clear from where such an additional 3-percentage-point decline in the offsetting factors will come.

In fact, it is quite plausible that some of the factors that have reduced interest rates in previous decades could begin to reverse and nudge interest rates even further upward.

Demographics. The large population of baby boomers who aggressively saved for retirement in their 40s, 50s, and early 60s have begun moving into retirement, where they will be expected to begin drawing down those savings. As will be discussed later, this is already happening in Japan, which has an older population than the U.S. [22]

Productivity. The rapid rise of computing technology represents the largest technological revolution in a century. Productivity initially soared in the 1990s as the technology became widespread, and has since lagged. This nonlinear productivity growth resulting from new technology should not be surprising, as the world continues to innovate, adapt, and learn new ways to apply these new resources. However, as long as research and development continue, the long-term productivity outlook should be positive. Relatedly, the contention that the world simply needs less capital investment is also questionable. Emerging economies are growing, and their expanded middle classes will require capital investments. Even in the U.S., new technologies will require regular upgrades, and even a gradual shift from fossil fuels to green technology will require significant new capital investments. Nor are traditional physical infrastructure needs going away.

Other Transitory Savings Factors. The global savings glut seems to have peaked in the mid- 2010s and is slowly receding. [23] The rate of private-sector deleveraging must also eventually slow down and stabilize.

Flight to Safety Weakens. Low interest rates on Treasury securities could induce borrowers to chase stronger returns elsewhere, such as the stock market or emerging economies.

Federal Reserve Policy. The Federal Reserve could be expected to raise short-term interest rates over time because of faster economic growth or any uptick in inflation. On the flip side, if central banks weaken their commitment to containing inflation, the resulting price volatility could induce borrowers to demand a higher inflation-risk premium. [24] Rising inflation rates can be difficult to reverse and can raise long-term market expectations of inflation. Such developments would reduce the “flight to safety” appeal of holding Treasury bonds.

“Unknown Unknowns.” The past two decades have included a major market crash, a housing crash and deep recession, and a global pandemic. Markets have long underestimated the probability of tail risks and “black swan events” that can roil markets. Wars, financial crises, pandemics, environmental catastrophes, cyberterrorism, or any number of unanticipated events can drive the economy in unanticipated directions, including raising or lowering interest rates.

Any of the variables above could conceivably push interest rates in either direction. However, it is worth reiterating that, as long as the projected doubling of the national debt (as a share of the economy) is likely to push interest rates upward by approximately 3 percentage points, the offsetting factors above would need to continue pushing interest rates downward by an additional 3 percentage points to maintain current interest rates.

Some of the factors affecting interest rates—Federal Reserve policy, quantitative easing, private- sector deleveraging, and the dampening effect of the pandemic recession—are likely transitory. Others, such as productivity, demographics, and the demand for capital investment, are longer-term structural factors—but there is no guarantee that they will continue on their current trends indefinitely.

According to the aforementioned economist Thomas Laubach, in an economy operating at its potential and with stable inflation rates, interest rates should revert to a natural equilibrium level (known as the R-star) that is largely related to output growth. Laubach noted that the R-star dropped over the past few decades because of changes in productivity, demographics, and global factors. If those variables reverse, so can the R-star. [25]