Don’t Bust the Cap: Problems with Eliminating the Social Security Tax Cap

"The Easy Solution?" Not So Much

(Originally published by the Manhattan Institute)

Introduction

Social Security’s deepening funding shortfalls are driving the system’s trust fund to within a decade from insolvency, which would mean an immediate 23% reduction in benefits. Social Security’s program deficits—which budget experts have warned for decades would occur as the 74 million baby boomers retire—remain largely ignored by politicians and political activists. However, when pressed for solutions, both progressives and an increasing number of nonprogressives claim to have a simple and obvious answer: apply Social Security’s 12.4% tax rate to all wages, rather than continue to limit this tax to an individual’s first $168,600 earned annually (this cap is the limit for 2024, and it automatically rises with inflation).[1] Eliminating the tax cap is not typically presented as a partial solution to Social Security’s budget shortfalls, to be combined with other policies such as raising the eligibility age or trimming upper-income benefits. Rather, this policy is often sold as a singular cure-all that would bring permanent Social Security surpluses and thus avert the need for any benefit or eligibility age hikes.

Such savings assumptions are vastly overestimated, according to consensus estimates. And the prospect of imposing a steep 12.4% tax-rate increase on families that would be considered upper middle class in many metropolitan areas is so unpalatable that even the leading progressive Social Security proposals by Senator Bernie Sanders (D–VT)[2] and Representative John Larson (D–CT)[3] would reimpose this tax only beginning at the higher wages of $250,000 and $400,000, respectively (and neither bill comes close to achieving solvency purely on this policy).

While some changes to the Social Security tax cap should certainly be on the table, eliminating the cap would provide smaller than expected savings while imposing a substantial, mostly unanticipated, burden on other federal funding priorities. This issue brief details the six main drawbacks of uncapping the tax.

The Drawbacks

1. Capping High-Earners’ Social Security Taxes Also Caps Their Benefits.

The current cap on Social Security taxes is not intended to be a giveaway to the rich. Because benefit formulas are directly tied to Federal Insurance Contributions Act (FICA) tax contributions, the $168,600 cap on taxable wages (which translates into a limit of $20,906 in Social Security taxes split between the employer and employee) also caps the amount of wages and taxes that can earn Social Security benefits. Uncapping Social Security’s wage base and taxes would also uncap the benefits that high-earning workers could earn.[4]

Even with the cap on taxes, high-earners receive a worse deal than low-earners. This is because—once lifetime wages are adjusted into current levels based on wage inflation—the initial Social Security benefit replenishes 90% of the first $14,088 in annual wages, then 32% up to the $84,936 level, and 15% of the remaining wages up to the taxable maximum (benefits are calculated based on monthly wages but are annualized here for illustrative purposes).[5] Thus, while typical high-earners will receive a larger initial Social Security benefit than low-earners, their return as a share of the lifetime Social Security taxes will be lower. Low-earners will see their Social Security benefits replace a larger share of their lifetime contributions than high-earners. Sure enough, a 2023 analysis by the Urban Institute shows that—measured by net present value—low-earners come out far ahead on Social Security, while some categories of high-earners will receive a net negative return on their lifetime program contributions.[6] Social Security formulas are already strongly progressive even with the tax cap.

Nevertheless, a common reform proposal would uncap Social Security taxes while canceling the corresponding benefit increase. Such a reform would fundamentally change the nature of the Social Security system. Social Security has always been presented as a social insurance program in which, as with a traditional pension, your benefits are “earned” by your level of tax contributions. Thus, Social Security’s benefit formulas have always ensured that future benefits rise alongside current tax contributions (albeit by a ratio that declines as wages and payroll taxes rise, as described above). If lawmakers completely de-link these new payroll taxes from earning any corresponding benefits, Social Security will function more like a traditional income-redistributing welfare program. De-linking contributions and benefits may be justified on fiscal grounds; yet such a move was opposed for decades by New Deal–inspired liberals who feared that converting Social Security more into a welfare system would undermine public support.

2. No, Eliminating the Cap Does Not Bring Permanent Solvency.

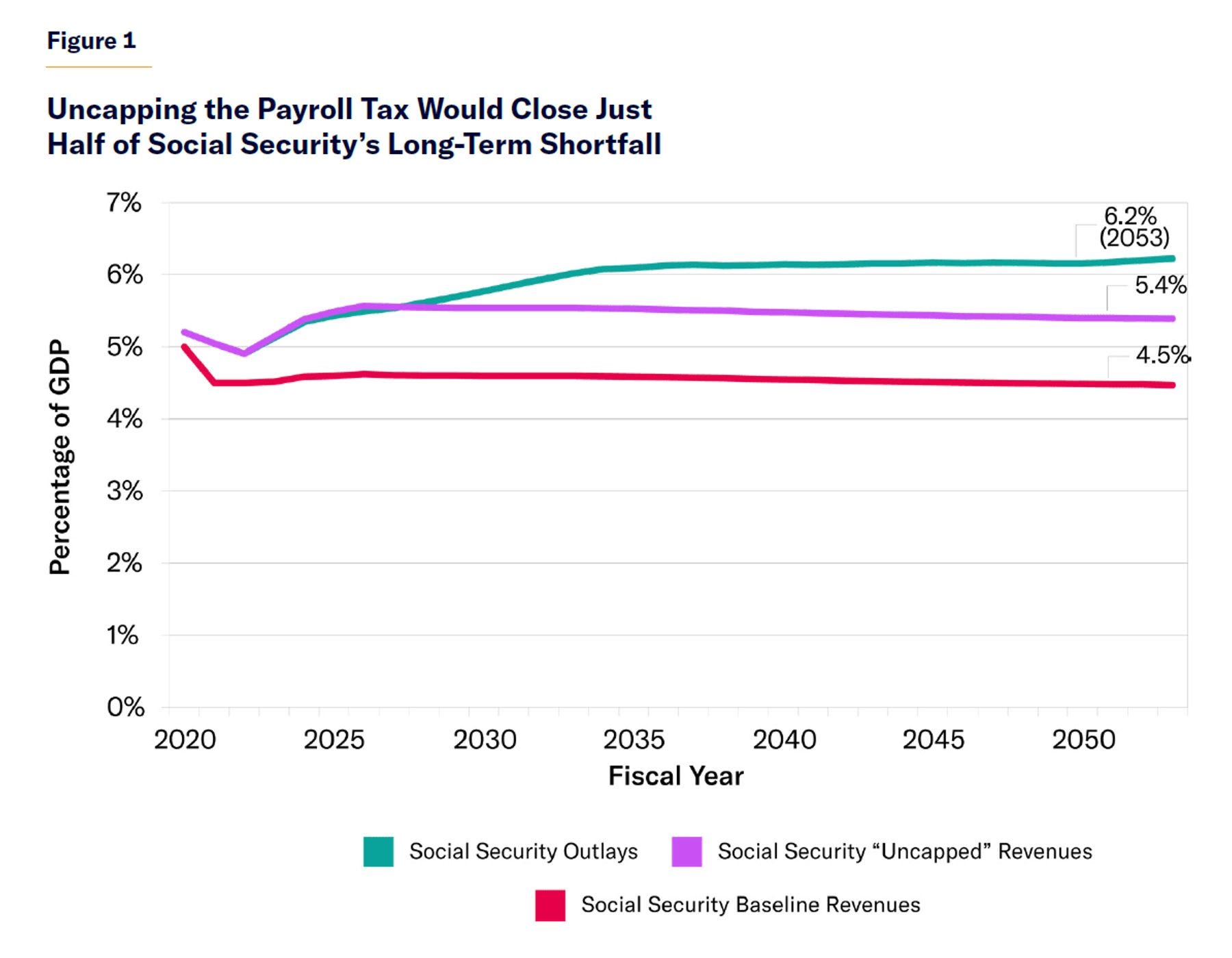

Advocates regularly overstate their case by relentlessly claiming that eliminating the cap will bring permanent solvency to Social Security and thus prevent any benefit cuts or eligibility age hikes. However, eliminating the cap would close only half of Social Security’s long-term shortfall.[7] Social Security spending is projected by the Congressional Budget Office (CBO) to level off at 6.2% of GDP over the long term.[8] Yet the Social Security trustees calculate that eliminating the cap would merely raise Social Security revenues from 4.5% to 5.4% of GDP—while also eventually nudging up spending levels by 0.1% of GDP because more payroll taxes automatically bring modestly higher long-term benefit levels.[9]

For a rule of thumb, the current Social Security tax raises 4.5% of GDP[10] by catching 83% of all wages in eligible jobs,[11] so catching 100% of wages would collect revenues of 4.5/0.83 = 5.4% of GDP. Thus, as Figure 1 shows, even eliminating the cap would not avert the need to raise the eligibility age and reform benefits.

3. Social Security Would Quickly Return to Deficits.

The Social Security trustees project that, even if the tax cap is eliminated, the system would fall back into deficit by 2029—just five years from now.[12] The trustees also show that the Social Security trust-fund exhaustion date would move out 21 years, to 2055.[13] However, the box below explains that the trust fund is an accounting mechanism that is largely irrelevant to Social Security’s finances. If those initial Social Security surpluses are not saved or used to pay down debt—a safe bet—then those Social Security deficits between 2029 and 2055 would still have to be financed by concurrent taxes or borrowing the same, as if no trust fund existed.

Is the “Raided” Trust Fund to Blame?

A common argument asserts that Social Security’s financial difficulties are simply the result of lawmakers raiding its $3 trillion trust fund. In reality, the trust fund was always just an accounting mechanism. It never contained real economic resources from which to pay benefits, and there was never any statutory mechanism for Congress to “save” the $3 trillion surplus that Social Security ran between 1983 and 2009. Instead, the Social Security Administration (SSA) was required by law to lend its surpluses to the Treasury to finance current government spending—with a promise that the Treasury (i.e., the taxpayers) would repay the Social Security system (with interest) down the road when it begins to run deficits. The balance of the Social Security trust fund is merely a running tally of how much of that $3 trillion loan has yet to be repaid to SSA by the Treasury and taxpayers. It is not a savings account with economic resources from which to pay the benefits.

But don’t take my word for it. Even President Obama’s FY 2017 budget proposal clarified that:

From the perspective of the Government as a whole, the trust fund balances do not represent net additions to the Government’s balance sheet…. When trust fund holdings are redeemed to fund the payment of benefits, the Department of the Treasury finances the expenditure in the same way as any other Federal expenditure—by using current receipts if the unified budget is in surplus or by borrowing from the public if it is in deficit. Therefore, the existence of large trust fund balances, while representing a legal claim on the Treasury, does not, by itself, determine the Government’s ability to pay benefits.[a]

Put another way, investing an initial Social Security surplus in Treasury bonds creates an asset for Social Security and an equal liability for the Treasury. Since both borrower and lender are part of the same federal government, the net effect on overall federal finances is to cancel each other out. Counting those Treasury bonds as net wealth is the equivalent of raiding one’s own retirement savings to go on vacation, writing yourself an IOU to repay your retirement fund later, and then treating that IOU as new net wealth to offset the cost of the vacation.

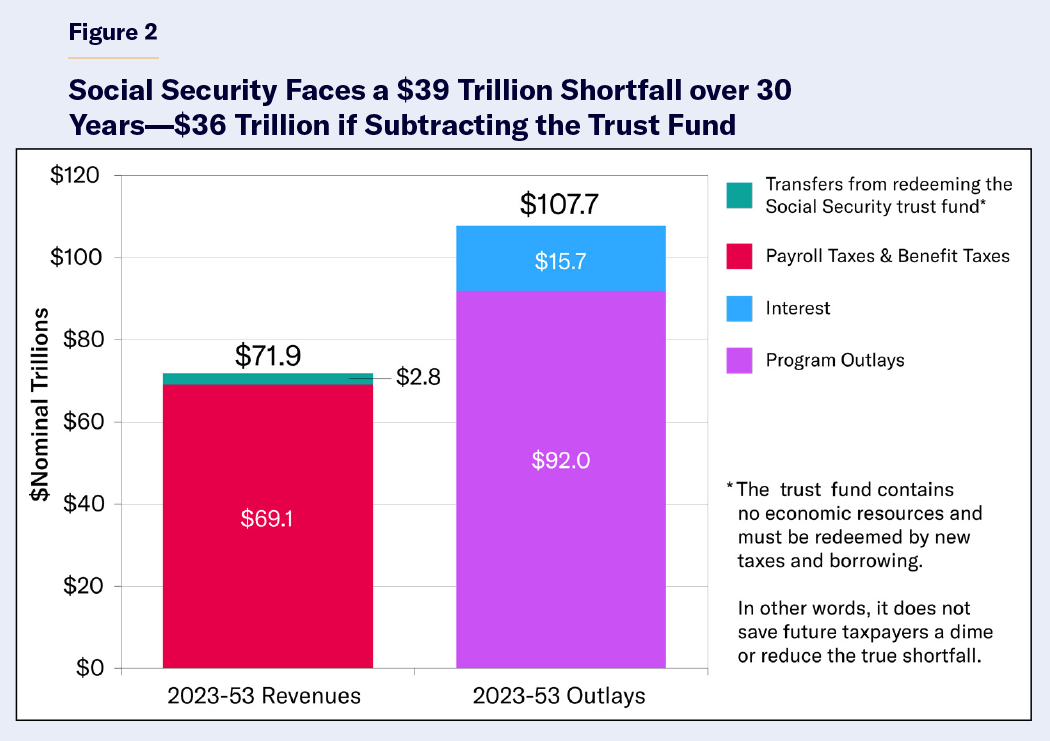

Setting aside the accounting minutiae, even if that $3 trillion Social Security surplus had been saved in the “lockbox,” it would finance only a small fraction of the $39 trillion Social Security shortfall ($23 trillion in program deficits plus $16 trillion in resulting budget interest costs) projected by CBO over the next 30 years (Figure 2).[b] The effect of the Social Security trust fund on the system’s long-term finances has been greatly exaggerated.

4. Even Canceling the Accompanying Benefit Hike Does Not Save Much.

Advocates of eliminating the tax cap often claim to ramp up the savings by canceling the additional Social Security benefits that—by current formula—would be paid out of some of those new taxes. However, in addition to undermining Social Security’s status as a social insurance program, such a reform would have no significant fiscal effect for the next several decades because the benefit-side changes resulting from uncapping FICA taxes are so small. Thus, the trustees estimate that canceling that benefit would still leave the system in deficit by 2029.[14] The trust-fund exhaustion date would move from 2055 to 2060—but again, that is mostly an accounting mechanism unless those earlier surpluses are saved.

The points above show that eliminating the payroll tax cap is not the cure-all that has been suggested and will not prevent the need for benefit and eligibility age changes. Still, many progressives might assert that even closing half of the Social Security shortfall would represent significant progress and reduce the amount of remaining savings required from other program reforms. However, the next two points show why eliminating the cap could be harmful to federal priorities.

5. It Would Use Up Nearly All Available “Tax-the-Rich” Revenues.

Most progressives (and even many nonprogressives) vastly overestimate the amount of tax revenues that could be raised from taxing the rich.[15] For example, even 100% tax rates on million-dollar earners would not come close to balancing the budget,[16] and seizing all $4.5 trillion of billionaire wealth—every home, car, business, and investment—would merely fund the federal government one time for nine months.[17]

Currently, the marginal tax rate on wages for the highest-earning Americans exceeds 50% when including the 37% federal income-tax rate, 2.9% Medicare payroll tax, 0.9% additional Medicare tax, and state income taxes that can surpass 10% in states with high concentrations of millionaires (and rise as high as 13.3% in California). Uncapping the payroll tax would add a 12.4% tax-rate increase for higher earners, pushing the top marginal rates well into the 60s. Given the economist consensus that the revenue-maximizing tax rate on labor income is 50%–73% (with marginal tax revenues quickly declining toward zero as tax rates approach the peak level), this policy clearly would leave no additional room to raise tax rates on wealthy families.[18] Note that investment tax rates are also near revenue-maximizing levels, a wealth tax is almost certainly unconstitutional, and the mortgage interest and state and local tax deductions have already been aggressively capped. America’s corporate tax rates remain higher than those of most competitors, and the plausible corporate tax hike revenues pale in comparison with Washington’s long-term budget deficits and new funding proposals.[19]

This means that—with the exception of a few modest tax tweaks—uncapping the payroll tax to finance Social Security would leave no pot of potential tax-the-rich revenues to close Medicare’s much larger funding shortfall (rising to 3.7% of GDP over three decades).[20] Nor could taxes on wealthy families finance much of the progressive wish list such as climate-change mitigation, free college, student loan forgiveness, health-care coverage expansions, K–12 education, infrastructure, child care, family leave, safety net, and housing. Progressives would need to sell (strongly unpopular) middle-class taxes to finance the rest of their agenda, as well as to address the massive Medicare shortfalls that will drive deficits steeply upward.

6. Are Wealthy Baby Boomers the Most Deserving Recipients of the Limited Remaining “Tax-the-Rich” Revenues?

Given the more pressing progressive priorities listed above (as well as growing baseline deficits driven by Medicare shortfalls and the remaining Social Security gap), directing nearly all remaining tax-the-rich revenues to baby-boomer Social Security benefits would be a curious choice. It would be especially surprising since today’s retirees are the wealthiest age group of Americans in history, with household incomes that have grown four times as fast as those of the average worker since 1980.[21] In fact, because most retirees are wealthier than the taxpayers financing their benefits, Social Security today largely redistributes income upward, not downward. Of course, many seniors still struggle (which can be more affordably addressed by hiking the minimum benefit), yet pledging that today’s workers will pay any tax necessary to ensure that even multimillionaire seniors can continue to receive benefits far exceeding their lifetime Social Security contributions is neither progressive nor sensible.

In fact, raising Social Security taxes (rather than addressing benefits) would accelerate the largest and most inequitable intergenerational wealth transfer in world history. Over the next 30 years, working families are on the hook to finance $164 trillion in Social Security and Medicare benefits for seniors (plus $47 trillion in interest costs resulting from these programs’ shortfalls).[22] Paying all promised Social Security and Medicare benefits would require—in addition to eliminating the Social Security tax cap—eventually raising the payroll tax rate by 8 percentage points plus imposing a 10% value-added tax. This burden would merely ensure that the wealthiest generation receives Medicare benefits more than triple their lifetime Medicare taxes (adjusted for net present value) and that they also come out ahead by 6% on Social Security.[23]

At least when working European families pay exorbitant tax rates, they immediately receive the benefits back through a healthy safety net. American workers will pay all these taxes to finance retirees, on the hope that perhaps the system will still be around decades later when they retire.

A more progressive reform would scale back the unaffordable (and, in many cases, not fully earned) spending promises made to wealthier baby boomers and save any future tax-the-rich revenues for higher progressive priorities.

Conclusion

Social Security’s growing shortfalls and looming trust-fund insolvency require the consideration of a broad range of savings policies. No single policy—including lifting the Social Security tax cap—can fix the entire shortfall without the need for other savings proposals. And while fully eliminating the cap could close half the long-term shortfall, advocates should note that such a policy would dramatically raise taxes not just on the rich but also the upper middle class. It would also rob nearly all other progressive priorities (and the larger Medicare shortfalls) of their largest potential tax-the-rich funding mechanism—all to ensure that (mostly) wealthy baby boomers receive benefits vastly exceeding their lifetime contributions to Social Security. Generational equity requires scaling back the unaffordable promises made to current and future retirees, rather than maxing out the taxes on working families.