Cut Spending For The Rich Before Raising Their Taxes

A More Straightforward and Pro-Growth Approach

Members of Congress have increasingly demanded large tax hikes on upper-income families to finance large spending increases on top of soaring baseline deficits. But even the most aggressive tax hikes on the rich would make only a small dent in the long-term budget deficits, and they would significantly harm the economy. Before considering any new taxes, lawmakers should first reduce federal spending benefits for high-income families. This bipartisan strategy would achieve both the redistributive goals of the left and the spending restraint goals of the right.

Such upper-income spending cuts have several advantages over new taxes: 1) they will not harm economic growth, 2) they increase future policy flexibility, 3) they are better targeted, and 4) they promote political compromise.

Several programs target spending to wealthy Americans. This report focuses on three of the largest: Social Security, Medicare, and farm subsidies, where basic reforms could save upward of $1 trillion in the first decade, and substantially more in future decades.

Introduction

As structural budget deficits grow to trillions of dollars and politicians promise even more spending, taxing the rich has become a popular solution to finance expanded government. But large tax increases on high earners not only are insufficient to close much of these budget gaps; they would also reduce economic growth and kill jobs. Additionally, they are often poorly targeted, build expectations of higher government benefit levels later, and reduce Congress’s flexibility to tax these families for other purposes down the road.

The goal of redistributing income down the ladder can be accomplished not only by taxing the rich but also by cutting federal spending that disproportionately benefits them. This approach is more pro-growth and better targeted. It also represents a plausible bipartisan compromise between progressives who want the wealthy to bear more of the costs of government and conservatives who prefer to simply reduce its size.

The federal budget is growing rapidly. The national debt held by the public has increased from $5 trillion to $22 trillion since 2007, as a result of two deep recessions, $6 trillion in stimulus legislation (across both recessions), and $3 trillion in tax cuts, as well as annual (inflation-adjusted) increases in the cost of Social Security, Medicare, and Medicaid of just under $1 trillion per year.

The national debt held by the public is projected to soar to $35 trillion by 2030[1]—or $42 trillion, if President Biden’s entire campaign agenda is enacted.[2] This would leave the national debt at 130% of GDP, or one-quarter higher than at the end of World War II.

Even without any new legislation, the Congressional Budget Office (CBO) projects $104 trillion in new borrowing over the next 30 years, bringing the national debt to 195% of GDP.[3] Nearly all this debt will result from general revenue transfers into the Social Security and Medicare systems to close their widening shortfalls, as well as the added interest costs on the national debt created by these shortfalls.[4]

Some new taxes on the rich will likely be part of any realistic plan to substantially close this gap.[5] But these taxes alone won’t come close to stabilizing the national debt. Hypothetically seizing all annual household income earned in America above the $1 million threshold would not even balance the short-term budget, much less address growing long-term budget gaps or finance new spending programs.[6 ]Even if we were to double the top two income-tax rates to 70% and 74%, impose the world’s largest wealth tax, tax capital gains as ordinary income, impose a 77% estate tax, and apply the Social Security payroll taxes all the way up the income ladder—bringing marginal income-tax rates of nearly 100% and savings taxed at similar rates—it would still not fully finance President Biden’s spending agenda, much less the underlying $100 trillion in borrowing that is scheduled in the baseline.[7]

Lawmakers should take a stronger look at cutting spending on the rich. While most federal benefits go to the middle class (particularly in the Social Security and Medicare programs) and federal antipoverty spending has steadily grown to 4% of GDP, Washington continues to distribute cash and in-kind federal benefits to wealthy families. Cutting this spending brings several advantages over upper-income tax hikes.

Economic Growth. While economists debate the magnitude of these effects on the margin, the general consensus is that steep tax-rate increases reduce incentives to work, save, invest, and be productive. They distort economic decision-making, incentivize expensive avoidance and evasion schemes, and often drive income away from the jurisdictions doing the taxing. Even if, as many economists believe, these costs can be outweighed by the benefits of federal redistribution programs or public goods, it would still be best to minimize those costs as much as possible. Reducing upper-income spending benefits can enhance redistribution yet avoid many of the broader negative macroeconomic effects of large new taxes.

Policy Flexibility. High taxes reduce policy flexibility in two ways. First, tax rates can rise only so high before the economic harm becomes overwhelming and new revenues fall away. For example, applying the 12.4% Social Security tax to all wages would close roughly half the long-term Social Security shortfall.[8] It would also raise combined marginal tax rates (including federal income, state income, and payroll taxes) on upper-income families past 60% in many states, which approaches the revenue-maximizing tax rate, and thus leaves little room for taxes on the wealthy to close the much larger Medicare shortfall or to finance new government initiatives on such things as climate, infrastructure, health, the safety net, K–12 education, and college student debt relief.

Second, exorbitant tax increases create expectations of large future government benefits, especially for social insurance programs. And the more that government locks in these large benefits, the more politically difficult it will be to unwind or repeal those benefits down the road as costs escalate. Maximizing tax rates and locking in unaffordable spending promises would paralyze future governments.

Better Targeting. The person paying the high tax rates today may not be around to collect the earned government benefits later. This problem would not apply to paring back spending benefits.

Political Compromise. Spending cuts are never popular. Yet many wealthy families would surely accept smaller current and future government benefits in return for limiting the substantial tax increases that they may otherwise face. Additionally, conservatives wary of tax increases may be willing to accept the progressive goals of expanding redistribution through this alternative route.

Critics of these cuts will contend that programs like Social Security and Medicare enjoy broad support because they are universal, and thus any means-testing will render them as unpopular (and prone to cuts) as welfare. But means-tested programs have proved extraordinarily politically resilient. Since 1965, federal antipoverty spending has steadily risen from 0.5%–4.0% of GDP[9]—across Republican- and Democratic-led governments—and programs like Medicaid have been expanded with the strong support of state referenda. Nor is it true that these programs are entirely universal; Medicare benefits, for example, have been income-related, without undermining program support. It is not true that means-testing will lead to drastic, across-the-board cuts.

Furthermore, there is no reason to believe that large tax increases would not undermine program support among wealthy families just as much as benefit cuts. If wealthy people support Social Security because their taxes finance their future benefits, then doubling their Social Security taxes (by eliminating the payroll-tax wage limit) without a corresponding benefit increase will break that tax-to-benefit link just as much as cutting their future benefits. Social Security expert Andrew Biggs states: “It is not clear why large benefit cuts for high earners would reduce their support for entitlement programs, as the left believes, but even larger tax increases would not—unless we assume that the best-educated and hardest-working Americans are extremely bad at math.”[10] Once it is agreed that wealthy families should bear a larger burden of redistribution, higher taxes and smaller benefits both accomplish the same goal.

Several programs disproportionately benefit wealthy Americans. This report focuses on three of the largest: Social Security, Medicare, and farm subsidies, where basic reforms could save upward of $1 trillion in the first decade, and substantially more in future decades.

Why Subsidies to Wealthy Seniors Should Be Targeted

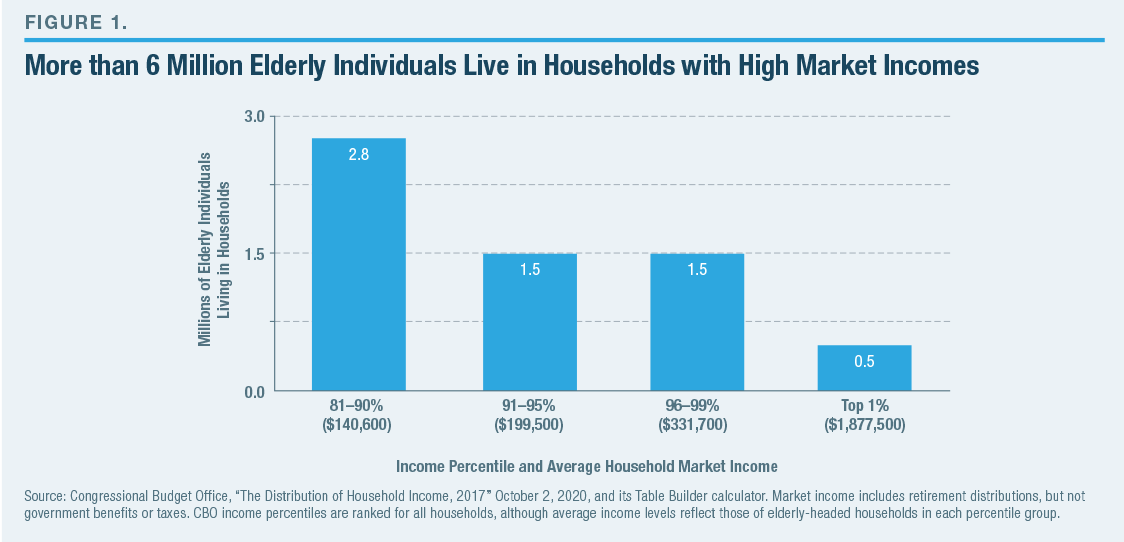

Social Security and Medicare were created in eras in which most senior citizens endured low incomes and little savings. By contrast, today’s seniors are the wealthiest cohort in the wealthiest country in its wealthiest era.[11] While some seniors still struggle, average household retiree income grew more than twice as fast as working-age salaries between 1979 and 2016 (the latest data available).[12] And the wealthiest 10%–20% of seniors are doing remarkably well. Four million retiree households hold more than $1 million in investable assets, and 1.1 million households hold more than $3.5 million.[13] Relatedly, CBO data show that 6.3 million elderly Americans live in households that currently earn annual market incomes of at least $87,200 for someone living alone or $123,400 for a two-person household—including 2 million seniors in households earning more than $174,100 (one person) or $246,200 (two people) annually (Figure 1). To the extent that such high post-retirement incomes derive from annuities or 401(k)-style investments, they suggest investment portfolios that are well into the millions of dollars.