Britain and France’s Debt Crises are Bad. America’s Will be Worse.

Washington’s fiscal failings mirror Europe’s economic mess

(Originally appeared in the Washington Post)

Washington’s spiraling debt trends are simply unsustainable. If you doubt this, consider the fiscal crises, protests and political chaos occurring beyond our shores.

Governments across the globe cumulatively spent on average $1.3 trillion annually on debt interest payments in the 2010s. Soaring debt and loan rates have escalated this year’s interest costs to $2.7 trillion. In five years, that number is projected to hit $3.9 trillion. This avalanche of borrowing costs represents the latest sign of long-term debt binges that have been mostly driven by aging populations and sluggish economies.

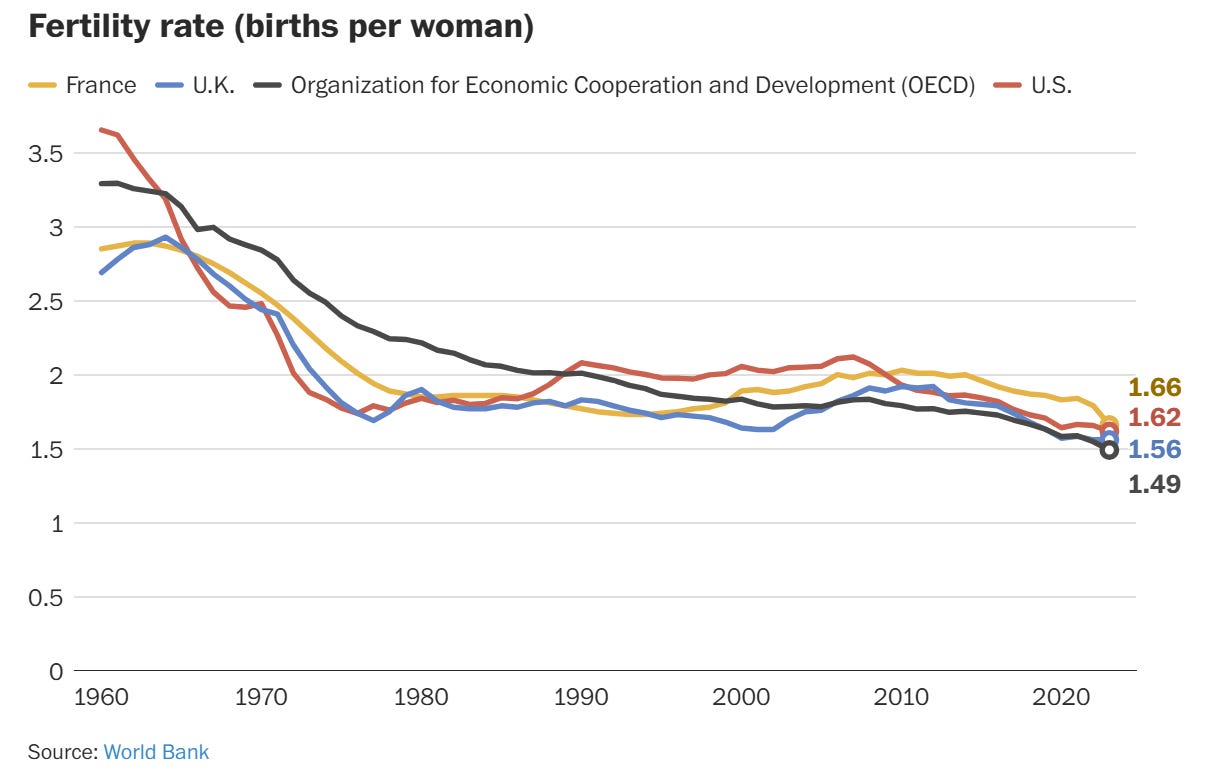

Let’s begin with Britain’s fiscal mess. The combination of aging baby boomers and falling fertility rates (now below 1.5 per woman) has swelled senior and health benefit costs beyond what its stagnant base of taxpaying workers can finance. Because economic growth is roughly the sum of labor force expansion and labor productivity increases, this workforce slowdown has strangled the British economy, especially with productivity trends also weak. Consequently, the economy has grown less than 2 percent annually since 2000 — and government forecasters see no improvement coming.

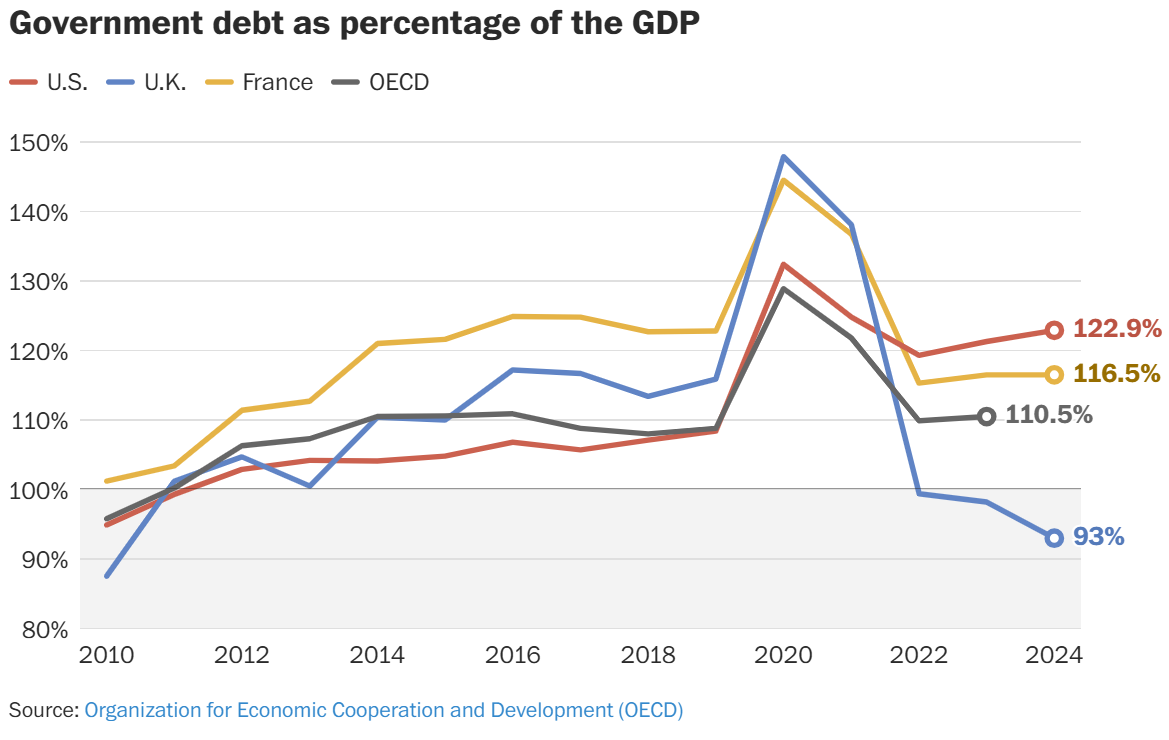

With the British economy failing to fund the benefit costs of its aging population, the resulting borrowing spree is being financed at the highest interest rates since the 1990s. This has pushed interest costs to almost 10 percent of public spending, nearly 50 percent higher than the defense budget. Britain’s Office for Budget Responsibility warns that the current debt — just less than 100 percent of its economy — is on its way to 270 percent within five decades, which would exceed the government’s reasonable borrowing capacity.

Yet the nation remains largely in denial. A historic tax increase enacted last year was plowed into government spending rather than closing the fiscal gap and a stubborn refusal to reform spending has brought calls for another tax hike.

At least the British government is still standing. France’s fiscal chaos has brought the current government’s collapse. The narrative is familiar. Aging baby boomers and a 1.7 fertility rate mean that France’s annual deaths are likely to begin outnumbering births by 2027 — forcing all net population increases to come from immigration, which itself faces political backlash. Also like its neighbor across the channel, France’s weak productivity and stagnant workforce size has limited economic growth to 1.2 percent annually over the past decade.

Within the European Union, only Greece and Italy exceed France’s debt, which stands at 116 percent of the gross domestic product and is heading to 130 percent within a decade. Annual interest costs are set to surge by two-thirds over five years and risk becoming the government’s most expensive budget item. Perhaps not surprisingly, Moody’s downgraded the French government’s credit rating last December.

The Macron administration initially attempted to supercharge its economy with even more borrowing for government investments and business tax relief. When this failed, a 2023 law raising the retirement age from 62 to 64 unleashed two weeks of nationwide protest, and recent calls for even modest austerity reforms caused the government to fold. Protests aside, French austerity is becoming economically unavoidable.

Yet neither France nor Britain can match the combination of debt unsustainability and denial in the United States, whose budget deficits are nearly $2 trillion and moving to $4 trillion within a decade. Within three decades, continuing current policies would propel annual deficits to 14 percent of the economy and the debt to nearly 250 percent of the economy.

The underlying drivers align with France and Britain.

First, the demographic challenge. The retirement of 74 million baby boomers combined with low fertility rates will drop workforce growth toward zero — leaving any population gains to come from (likely restricted) immigration. With fewer workers left to finance each retiree, Social Security and Medicare face a combined annual shortfall of $700 billion this year, rising to $2.2 trillion within a decade and totaling $122 trillion over three decades when including resulting interest costs.

Second, the economic challenge. Financing these retirement benefits requires a strong economic buildup. However, the slowdown in labor force and productivity trends has reduced annual economic growth to 2.1 percent since 2000. Worse, the Congressional Budget Office forecasts just 1.8 percent annual growth moving forward as labor force expansion trends toward zero.

America’s last hope was that — if an underperforming economy and tax revenue could not keep up with the accelerating costs of an aging society — Washington could at least plug the gap with cheap borrowing. In the 2010s, the government comfortably borrowed heavily because of low interest rates that the CBO projected would never exceed 4 percent. Unfortunately, this low-interest rate honeymoon eventually fell victim to rising inflation, tighter Federal Reserve policy and reduced global savings flows.

Closing that last door of ultracheap borrowing leaves no easy exit. America’s economy, workforce and tax code are not equipped to finance the expanding Social Security and Medicare shortfalls. France and Britain are at least debating solutions. The U.S. continues to slash taxes, add benefits and ignore unfathomable budget deficits. Yet the laws of math and economics always win eventually, and Americans are dangerously ill-prepared for what is coming.