A Blueprint for Sustainable Discretionary Spending Caps

Caps Constrain Spending - When Properly Designed

(Originally published by the Manhattan Institute

The recent enactment of statutory discretionary spending caps for FY 2024 and FY 2025 has revived the debate over the importance, efficacy, and design of discretionary spending caps. Within the next two years, Congress will debate whether to revise and extend those spending caps in order to address annual budget deficits that have doubled to nearly $1.5 trillion since 2018 and are projected to approach $3 trillion within a decade.[1] Discretionary spending, which has gradually fallen to 27% of total federal spending, is not the main driver of runaway deficits. But nonemergency discretionary appropriations have jumped by 23.4% in the past two years, adding $300 billion to current spending levels and raising the ten-year discretionary spending baseline by nearly $3 trillion.

The 2021 expiration of the discretionary spending caps of the Budget Control Act (BCA) has clearly led to a surge in “regular” (i.e., nonemergency) discretionary spending. However, even before expiring, BCA’s effectiveness was gradually weakened, as lawmakers repeatedly increased the caps. Additionally, the new 2024 and 2025 caps were accompanied by a concurrent bipartisan agreement to evade their spending levels in the later appropriations bills.[2] Therefore, future reimpositions of multiyear discretionary spending caps must be informed by the successes and failures of earlier caps.

History has shown that, paradoxically, overly ambitious discretionary spending caps that attempt to constrain spending too tightly will ultimately backfire and bring larger spending increases than less tight caps. Modest spending caps that accommodate realistic appropriations growth rates have sustainably reduced discretionary spending as a share of the economy. By contrast, caps requiring drastic cuts, or little to no annual spending growth, have typically been disregarded by Congress (or abused through loopholes) and replaced with appropriations hikes exceeding 10%. Because spending caps can be easily repealed at any time, they cannot force spending cuts beyond the political system’s capacity. They can only enforce an existing broad commitment to constrain spending.

Discretionary spending is not the lead driver of deficits, but it is typically the first place that Congress looks for deficit reduction. In fact, the six largest deficit-reduction laws since 1983 have cumulatively produced 53% of their savings from discretionary spending.[3] Preventing discretionary spending from growing faster than the economy is a necessary piece of the deficit-reduction puzzle. This report shows how Congress can best design sustainable caps on discretionary appropriations.

Discretionary Spending Background

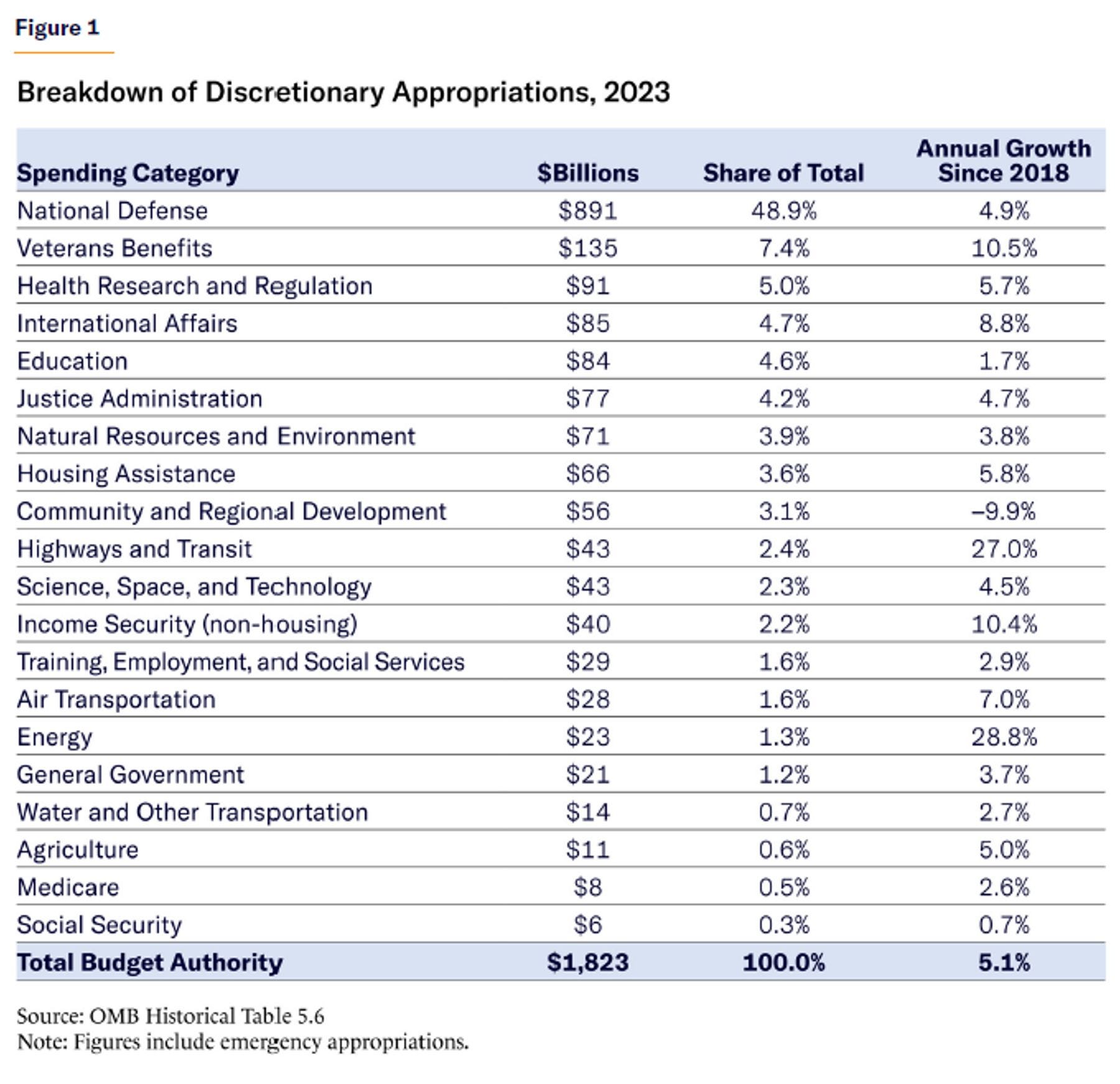

Virtually all federal spending programs are classified as either discretionary or mandatory. The spending levels for discretionary programs are set directly by Congress and the president through the annual appropriations process. Defense constitutes nearly half of discretionary spending, which also includes most spending on veterans’ health, K–12 education, health research, NASA, international assistance, and justice (Figure 1).

By contrast, spending levels for mandatory programs (mostly entitlement programs) are set by occasional authorizing legislation. For programs such as Social Security, Medicare, farm subsidies, and most antipoverty spending, Congress sets eligibility and benefit formulas, and then spending levels are determined by how many people enroll and where they fit into the benefit formula. Social Security, Medicare, and Medicaid have permanent authorizations, meaning that their underlying parameters never expire and are changed only when Congress and the president so desire, while other mandatory spending programs—as well as their eligibility and benefit formulas—are typically reauthorized by Congress on a schedule between two and seven years.

Because Congress does not set mandatory program spending levels (with a few minor exceptions),[4] these programs are often described as “uncontrollable” or “on autopilot.” Costs rise rapidly with program participation because of eligible population growth. At the same time, benefit formulas automatically rise each year; and occasionally, Congress passes legislation further expanding eligibility and benefit parameters. Because mandatory programs are not appropriated annually, Congress has little reason to provide oversight, address waste, or subject these programs to broader budget targets. Overall mandatory spending—excluding net interest costs on federal debt—has leaped from 5% to 15% of GDP since 1962.[5] And it is projected to continue rising indefinitely, driven entirely by escalating Social Security, Medicare, and Medicaid costs.

Discretionary spending levels, on the other hand, must be reappropriated annually and are subject to regular oversight when there is a spending target to meet. Increasingly crowded out by mandatory spending growth, discretionary spending has fallen from 67% to 27% of federal outlays since 1962.[6] During this period, discretionary outlays as a share of GDP decreased from 12.3% to 6.6%, bottoming out at 6.0% in 1999.[7]

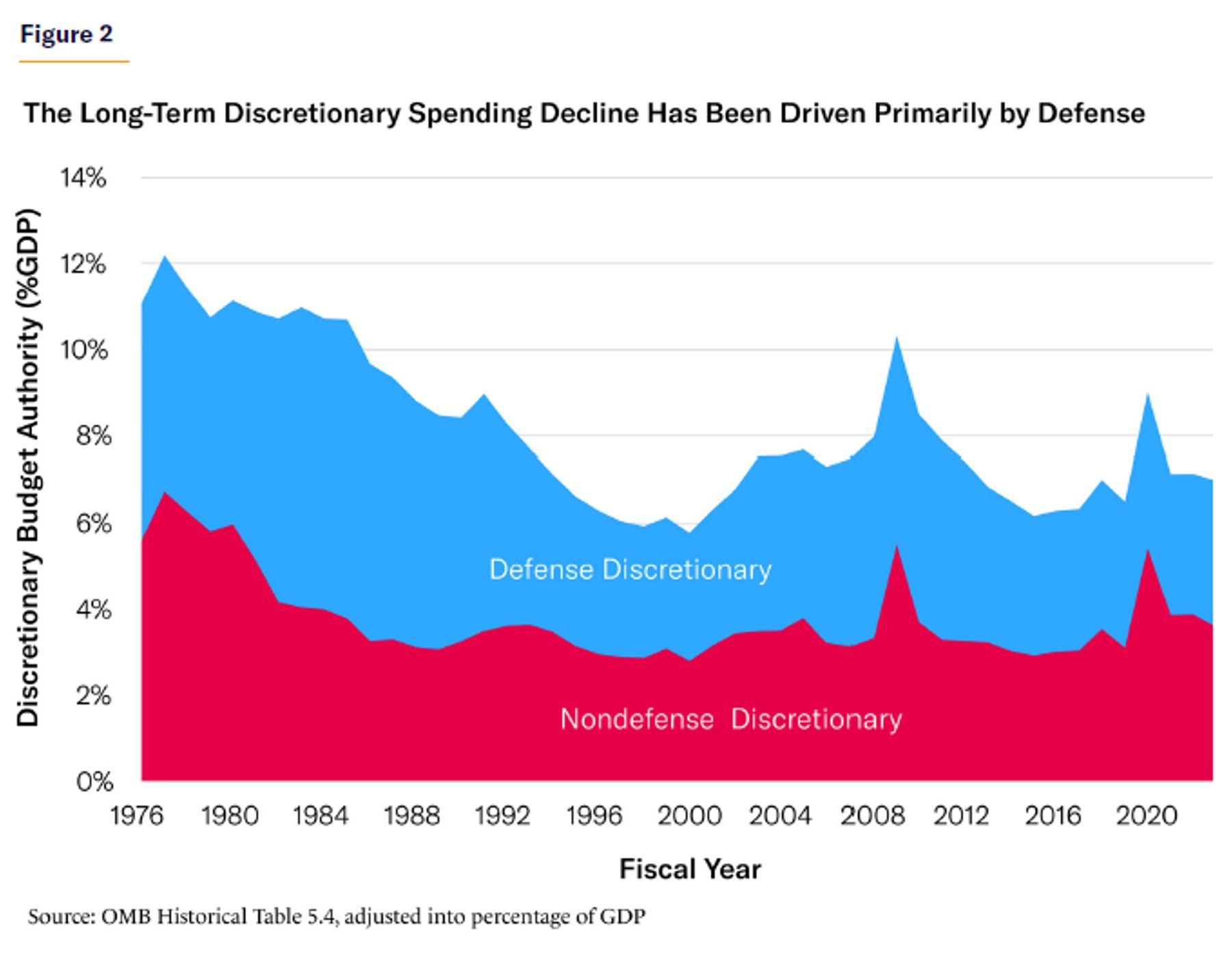

The decline in discretionary spending has been driven by defense spending. Its share of the economy gradually fell from 9% in the early 1960s, to 3% shortly before the 9/11 attacks, which brought a rebound to 4.6% by 2010, before falling back to 3% by 2023 (Figure 2).

Nondefense discretionary spending levels have remained steadier, typically ranging between 3.0% and 4.5% of GDP, with a current level of 3.6% of GDP. Still, since 1990, nondefense discretionary spending (after inflation) has expanded by 154%, versus 35% for defense.[8]

Thus, while discretionary spending has not been the driver of rising long-term deficits—and cannot realistically be cut deeply enough to accommodate surging mandatory costs—Congress should still approach this spending with a “do no harm” principle, ensuring that it does not rise as a share of the economy and further deepen the surging baseline budget deficits.

The Modern History of Discretionary Spending Caps

Statutory discretionary spending caps were born from the failure of broader deficit-reduction targets. In 1985, rising deficits led Congress and President Ronald Reagan to enact the Balanced Budget and Emergency Deficit Control Act of 1985 (nicknamed “Gramm-Rudman-Hollings” [GRH], after its lead Senate authors). The law set declining annual deficit targets—enforced by automatic cuts of any overages, known as “sequestrations”—that aimed to eliminate the budget deficit by 1991. A Supreme Court decision forced Congress to rewrite the law in 1987, which pushed the target balanced-budget date to 1993.[9]

GRH modestly restrained spending and deficits. However, the law was also sabotaged by typical congressional and White House shenanigans: exempting certain policies, tweaking economic assumptions, and blocking enforcement of deficit targets. More damaging, however, was GRH’s lack of flexibility to accommodate temporary deficit increases brought on by non-legislative changes such as a recession.[10]

In late 1990, with a weakening economy pushing up deficits and threatening a large sequestration, President George H. W. Bush and congressional leaders replaced GRH with the Budget Enforcement Act (BEA), as well as new legislation to raise taxes and trim mandatory spending.[11] BEA imposed multiyear caps on discretionary appropriations and imposed Pay-as-You-Go (PAYGO) rules blocking, via sequestration, new mandatory spending or tax legislation that would collectively widen projected budget deficits.

BEA represented a different approach from GRH in two key ways. First, while GRH was designed to spur future legislation to reduce baseline deficits, BEA was intended to protect concurrent deficit-reducing legislation from future repeal. PAYGO would limit Congress’s ability to repeal the budget deal’s tax increases and mandatory spending savings (or hike deficits through other tax cuts or mandatory expansions). The five-year discretionary spending caps would codify the existing bipartisan commitment to pare back the growth of appropriations. In short, while GRH was offensive (motivating future deficit reforms), BEA was defensive (protecting past deficit reforms).

Second, by limiting only new deficit-expanding legislation—PAYGO applied only to newly legislated expansions—BEA did nothing to limit the automatic baseline growth of mandatory spending due to pre-1990 program rules. Nor did BEA impose any constraints on automatic deficit fluctuations resulting from booms, recessions, and the business cycle.